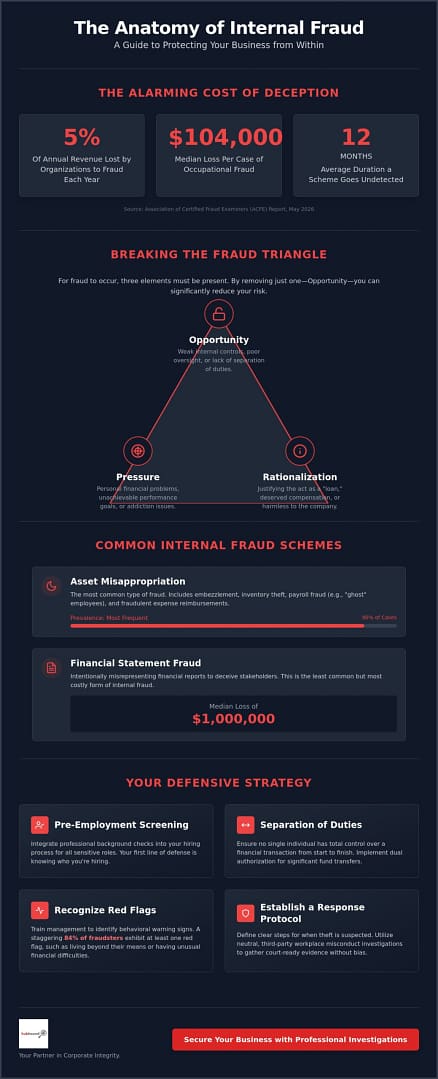

Did you know that organizations lose an estimated 5% of their annual revenue to fraud every single year? According to the May 2026 ACFE report, the median loss per case sits at $104,000, and most schemes go undetected for an average of 12 months. Discovering that a long-term employee has been siphoning funds is a professional betrayal that often leads to significant financial anxiety. Learning how to protect my business from internal fraud is no longer optional; it’s a critical requirement for maintaining operational integrity in an era of increasingly sophisticated misconduct.

It’s understandable to worry about the legal repercussions of an improper investigation or the potential for undetected embezzlement to cause total ruin. This article provides the professional investigative strategies and internal controls you need to shield your organization from loss. We’ll walk through the latest 2026 Nacha operating rules for ACH fraud monitoring, explain when it’s time to engage professional workplace misconduct investigations, and outline how to gather court-ready evidence. By the end of this guide, you’ll have a clear roadmap for securing your assets and identifying behavioral red flags before they escalate.

Key Takeaways

- Identify modern fraud vectors created by digital workflows and remote access to secure your organization’s financial perimeter.

- Disrupt the “fraud triangle” by implementing rigorous oversight and recognizing behavioral red flags that indicate external financial pressure.

- Apply the principle of separation of duties and dual authorization to ensure no single individual has total control over significant fund transfers.

- Learn how to protect my business from internal fraud by integrating professional pre-employment background checks into your hiring process for all sensitive roles.

- Establish a clear response protocol for suspected theft that utilizes third-party workplace misconduct investigations to ensure evidence is court-ready and neutral.

Understanding the Landscape of Internal Fraud in 2026

Internal fraud involves any deceptive act an employee commits for personal gain at your company’s expense. In 2026, the risk has evolved significantly. Remote access and decentralized digital workflows provide new vectors for misconduct that traditional oversight often misses. Small and mid-sized businesses frequently become primary targets because they rarely have the robust internal audit departments found in global corporations. Understanding these risks is the first step in learning how to protect my business from internal fraud.

Most cases fall into three distinct categories. Asset misappropriation is the most frequent, appearing in 90% of cases according to the May 2026 ACFE report. This often involves Embezzlement or the theft of physical inventory. Financial statement fraud is rarer but far more devastating, with median losses reaching $1 million. Finally, occupational fraud covers the broad spectrum of using one’s position for illicit enrichment. Vigilance is required as fraudsters now use generative AI to create realistic fake invoices or bypass basic digital security protocols.

The Financial and Reputational Cost of Misconduct

Direct financial theft is only the surface of the problem. When fraud occurs, it damages your brand’s reputation with vendors, clients, and investors. It also poisons employee morale. If staff members see a peer getting away with theft, a “contagion” effect can take hold, leading to widespread ethical decay. Beyond internal culture, you face legal and regulatory consequences for failing to maintain fiduciary oversight. This is especially true under the proposed 2026 Sarbanes-Oxley Act updates that emphasize management’s responsibility for internal controls.

Common Types of Internal Fraud to Monitor

Identifying specific schemes requires a selective filtering process. You should focus your monitoring on high-risk areas where oversight is often lax. Watch for these common patterns:

- Payroll fraud: This includes “ghost employees” on the ledger or unauthorized bonus payments routed to personal accounts.

- Expense reimbursement: Look for duplicate receipts or inflated travel claims that exploit loose approval digital workflows.

- Inventory theft: This involves manipulating supply chain records to hide the physical removal of goods or materials.

One of the most effective ways to mitigate these risks early is through rigorous pre-employment background checks. Screening candidates before they have access to your accounts prevents many issues before they start. Knowing how to protect my business from internal fraud starts with knowing exactly who you are bringing into your organization.

The Mechanics of Misconduct: Breaking the Fraud Triangle

To understand how to protect my business from internal fraud, you must first dismantle the psychological and structural drivers behind employee theft. Criminologists identify three elements that must converge for fraud to occur: opportunity, pressure, and rationalization. This framework, known as the Fraud Triangle, suggests that removing even one side of the triangle can prevent the majority of misconduct cases. While you cannot always control an employee’s external pressures, you have total authority over the opportunities presented within your organization.

Opportunity arises when internal oversight is weak or non-existent. Even traditionally honest employees may cross the line if they believe their actions will go unnoticed. Implementing Good Internal Control Practices is the most effective way to collapse this side of the triangle. By establishing clear audit trails and rigorous technical checks, you signal that every transaction is monitored. Pressure and rationalization are the human elements of the equation. Pressure often stems from personal financial crises, while rationalization allows the individual to frame the theft as a “loan” or “rightful compensation.”

According to the May 2026 ACFE report, 84% of fraudsters exhibit at least one behavioral red flag before they are caught. Recognizing these signals early is vital for any business owner. If you suspect irregularities, initiating professional workplace misconduct investigations can help you identify the specific side of the triangle currently at play in your office.

Identifying Behavioral Red Flags in Staff

Data-driven monitoring must be paired with human observation. Watch for employees who are suddenly reluctant to take vacations or share their financial responsibilities with colleagues. This behavior often masks a fear that a substitute will discover manipulated ledgers. Other red flags include sudden, unexplained changes in lifestyle or spending habits that don’t align with an employee’s known salary. Defensive behavior when questioned about minor financial discrepancies or reports is another common indicator of underlying issues.

Creating a Culture of Accountability and Transparency

A robust defense requires more than just software; it needs a cultural foundation. Establish a clear, written code of ethics and a zero-tolerance policy for any form of deception. Since tips account for 43% of fraud detection cases, implementing an anonymous whistleblowing hotline is a high-value strategy. Leadership must model this ethical behavior and fiscal responsibility at every level. When employees see that the rules apply to everyone, the psychological “rationalization” of fraud becomes much harder to maintain. This transparency is a cornerstone of how to protect my business from internal fraud effectively.

Essential Internal Controls and Separation of Duties

The most effective way to collapse the “opportunity” side of the fraud triangle is through the strict implementation of Separation of Duties (SoD). This principle ensures that no single employee maintains control over a financial transaction from initiation to completion. For example, the person who approves a vendor invoice shouldn’t be the same person who executes the payment or reconciles the bank statement. This structural friction is a primary answer to how to protect my business from internal fraud. By requiring multiple touchpoints, you create a system where collusion is necessary to bypass controls, significantly increasing the difficulty for a lone bad actor.

Implementing dual authorization for all significant fund transfers is another non-negotiable standard. In 2026, new Nacha operating rules require enhanced, risk-based fraud monitoring for ACH transactions. Your internal workflows should mirror these requirements by mandating that a second authorized user validates any high-value outbound payment. This redundancy is a core part of how to protect your business from occupational fraud and ensures that digital errors or malicious entries are caught before funds leave the organization. Since the typical fraud case lasts 12 months before detection, these layers of defense are your best chance at early intervention.

Implementing Robust Financial Oversight

Divide your financial responsibilities into three distinct categories: authorization, execution, and recording. When these roles overlap, the risk of asset misappropriation, which occurs in 90% of cases according to May 2026 ACFE data, increases dramatically. Ensure that bank statements are reconciled independently by a non-signatory. Use modern accounting software to track immutable audit trails. These digital footprints flag anomalous transactions or back-dated entries that warrant immediate review. Consistent oversight is a fundamental pillar of how to protect my business from internal fraud.

The Role of Regular Audits and Spot Checks

Internal reviews are necessary, but they shouldn’t replace unannounced spot checks. Surprise audits act as a powerful psychological deterrent. Employees are less likely to manipulate records if they know a review could happen at any moment without warning. During these checks, verify vendor information to identify “shell company” schemes where funds are diverted to fake entities. Additionally, enforce mandatory vacation policies. Many concealment schemes require the fraudster’s constant presence to “manage” the books. When that person is away, the lack of active maintenance often causes the scheme to unravel.

Investigative Due Diligence: Preventing Fraud Before It Starts

While internal controls provide a structural defense, they often fail to address the human element of risk. Many business owners rely on standard HR software to screen new hires, but these automated systems frequently miss critical red flags. These tools often rely on outdated or incomplete databases that don’t capture the full scope of a candidate’s history. To understand how to protect my business from internal fraud, you must look beyond basic digital scrapes. Professional investigative due diligence ensures that the individuals managing your capital are as reliable as the systems they use.

A high-value strategy involves implementing pre-employment background checks for every role with financial access. These aren’t just formality checks; they’re essential risk mitigation tools that filter out high-risk applicants before they enter your environment. Your responsibility doesn’t end on the first day of work, either. Continuous monitoring is necessary because external pressures like debt or lifestyle changes can occur at any point in an employee’s tenure. This proactive approach extends to external partners through thorough corporate due diligence on vendors and service providers.

Advanced Pre-Employment Background Screening

Don’t settle for surface-level validation. Verify all educational credentials and prior employment history directly to identify discrepancies that automated tools might overlook. Conduct deep-dive criminal record searches across multiple jurisdictions to ensure a clear history. For roles with significant fiduciary responsibility, assess financial stability. An employee under extreme personal financial strain is statistically more likely to succumb to the “pressure” side of the fraud triangle discussed in previous sections. Identifying these vulnerabilities early allows you to make informed hiring decisions based on verified data.

Identifying High-Risk Vendor Relationships

Internal fraud often involves collusion with external entities. Verify the physical existence and actual ownership of every new vendor before authorizing payments. Check for hidden conflict of interest links between your staff and service providers. Use investigative skip tracing to locate the principals behind suspicious entities. If you find a vendor with a residential address or a lack of verifiable business history, investigate further. This level of scrutiny is a cornerstone of how to protect my business from internal fraud by closing the loop on procurement risks.

Building a secure organization requires a selective filtering process for both people and partners. Secure your hiring pipeline today by ordering professional Pre-Employment Background Checks to verify every candidate’s integrity.

Responding to Suspected Fraud with Professional Investigations

Suspecting a long-term employee of theft is a high-stress scenario that requires immediate, calculated action. Don’t act on impulse. Confronting a suspect without a mountain of verified evidence often leads to the destruction of records or significant legal blowback. Learning how to protect my business from internal fraud includes knowing exactly how to react when your internal controls are breached. Your priority is to secure digital and physical evidence before it can be altered. Engaging a third-party expert ensures the neutrality required for legal standing in future proceedings. Professional workplace investigations provide a necessary buffer, shielding your organization from costly wrongful termination lawsuits.

A selective filtering process is just as important during an investigation as it is during hiring. You must follow a strict protocol to maintain the integrity of the case. Consider these essential steps:

- Do secure all digital logs and financial records immediately.

- Don’t confront the employee until you have verified, documented evidence.

- Do engage a neutral third party to lead the inquiry and maintain objectivity.

- Don’t access an employee’s personal devices or belongings without explicit legal clearance.

Gathering Court-Ready Evidence Through Surveillance

Confirming misconduct requires more than just a suspicion. Discreet surveillance operations are often the only way to catch a bad actor in the act. Whether the theft involves physical inventory or digital asset misappropriation, maintaining a strict chain of custody for evidence is non-negotiable. If you fail to document who handled the evidence and when, it won’t be admissible in court. Utilize high-definition video and unalterable digital logs to create a definitive timeline of unauthorized activities. This level of detail turns a “he-said, she-said” dispute into an open-and-shut case.

The Importance of Professional Witness Interviews

Evidence provides the facts, but interviews provide the context. Professional investigators use objective, non-coercive techniques to interview staff members who may have witnessed the fraud. These interviews must be handled with extreme care to avoid claims of intimidation or harassment. The goal is to transform verbal admissions into signed, legally binding statements that can withstand judicial scrutiny. Coordinate every investigative step with legal counsel to ensure total compliance with national labor laws. This comprehensive approach is the final piece of the puzzle in how to protect my business from internal fraud while preserving your professional reputation.

Securing Your Organization Against Internal Threats

Protecting your assets requires more than just updated software; it demands a culture of transparency and rigorous oversight. By breaking the fraud triangle through the separation of duties and dual authorization, you eliminate the easy opportunities that bad actors exploit. Integrating investigative due diligence into your hiring and procurement processes ensures that you only partner with verified, high-integrity individuals. Implementing these multi-layered strategies is the most effective way to understand how to protect my business from internal fraud while maintaining long-term financial stability.

When internal controls aren’t enough, professional intervention is necessary to secure your interests and prevent legal repercussions. Secure your business with professional investigative services from HubHound. Our licensed investigators bring over 30 years of industry experience to every case, providing court-ready evidence and professional witness statements. From comprehensive corporate due diligence to pre-employment background screening, we deliver the clarity you need to move forward. You don’t have to manage these risks alone. Take decisive action today to build a more resilient and secure organization.

Frequently Asked Questions

What are the most common signs of internal fraud in a business?

Behavioral red flags are the most reliable indicators of misconduct. According to the May 2026 ACFE report, 84% of fraudsters exhibit signs like living beyond their means or experiencing financial difficulties. You should also watch for operational anomalies, such as an employee’s sudden reluctance to take vacations or share financial responsibilities. These behaviors often mask active concealment schemes that require the fraudster’s constant presence to manage manipulated ledgers.

How can a small business implement internal controls on a budget?

Small organizations can achieve significant protection by implementing structural friction without high costs. Start by separating duties so no single person controls a transaction from start to finish. Mandate dual authorization for all outbound fund transfers and vendor payments. Enforcing a mandatory vacation policy is another high-value, low-cost strategy. Many schemes unravel when the person responsible is away and unable to maintain the fraudulent records.

Is it legal to conduct surveillance on an employee suspected of fraud?

Surveillance is generally legal in a professional workplace when it serves a legitimate business interest, such as investigating theft or misconduct. You must avoid areas where staff have a reasonable expectation of privacy, such as restrooms or changing areas. To ensure your evidence is admissible in court and doesn’t violate labor laws, always coordinate with professional investigators who specialize in surveillance operations and evidence collection.

What should I do first if I suspect an employee is stealing?

Your first priority is to secure all digital logs and physical financial records without alerting the suspect. Don’t confront the employee immediately; doing so often leads to the destruction of evidence and increases your legal liability. Contact a professional investigative firm to lead a neutral inquiry. This approach ensures you gather court-ready evidence and helps you understand exactly how to protect my business from internal fraud while avoiding wrongful termination claims.

Can pre-employment background checks really prevent internal fraud?

Rigorous screening is your first line of defense against high-risk hires. Professional background checks identify candidates with a history of financial misconduct or criminal records that standard HR software often misses. By filtering out individuals who have previously succumbed to financial pressure or shown a lack of integrity, you prevent the most common fraud vectors from entering your organization. This proactive due diligence is a cornerstone of long-term risk mitigation.

What is the ‘Fraud Triangle’ and why does it matter to my business?

The Fraud Triangle consists of three converging elements: pressure, opportunity, and rationalization. Pressure often stems from personal financial crises, while opportunity exists where internal controls are weak. Rationalization allows the employee to justify the theft as a temporary loan or rightful compensation. Breaking just one side of this triangle, typically by removing the opportunity through strict oversight, is the most effective way to learn how to protect my business from internal fraud.

Why should I hire a private investigator instead of doing it myself?

Professional investigators provide the neutrality and technical expertise required to build a legally sound case. They maintain a strict chain of custody for all evidence, ensuring it remains admissible in court if you pursue litigation. Third-party experts also protect you from claims of bias or harassment during witness interviews. Their involvement minimizes the risk of a botched investigation that could lead to a costly wrongful termination lawsuit or reputational damage.

How do I prove an employee is committing financial fraud?

Proving fraud requires a definitive timeline of unauthorized activities supported by immutable audit trails and digital logs. You must demonstrate clear intent and a pattern of deception, such as the manipulation of supply chain records or unauthorized bonus payments. Professional investigators enhance your proof by capturing high-definition surveillance footage and transforming verbal admissions into signed, legally binding witness statements. This comprehensive evidence package is essential for both civil recovery and criminal prosecution.