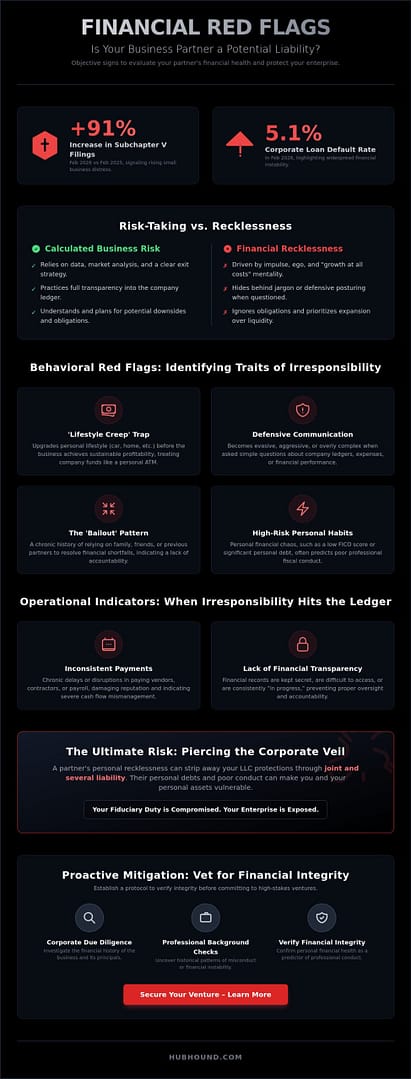

Did you know that Chapter 11 filings under Subchapter V saw a 91% increase in February 2026 compared to the same period in 2025? This surge in small business distress highlights a harsh reality: many companies aren’t failing because of the market, but because of internal instability. You likely feel a lingering anxiety that your partner’s “creative” accounting or personal spending habits are more than just quirks. It’s difficult to distinguish between standard startup pressure and the genuine signs of a financially irresponsible business partner when your own professional reputation is on the line.

We understand the fear of confrontation without hard evidence, especially when corporate loan default rates reached 5.1% in February 2026. This article provides the clarity you need to evaluate your partner’s financial health with objective precision. You’ll learn how to spot ten hand-picked behavioral red flags, understand the impact of the August 2026 LLC and partnership law amendments, and gain the confidence to initiate a professional background check or corporate due diligence investigation. This curated checklist ensures you can mitigate risk before a financial crisis forces your hand.

Key Takeaways

- Distinguish between temporary startup growing pains and chronic, systemic mismanagement to identify where true risk lies.

- Recognize the behavioral signs of a financially irresponsible business partner, including defensive communication about company ledgers and premature personal lifestyle upgrades.

- Identify operational red flags like inconsistent vendor payments or payroll disruptions before they evolve into tier-one legal crises.

- Protect your enterprise from joint and several liability by understanding how a partner’s personal recklessness can strip away your LLC protections.

- Establish a protocol for corporate due diligence and professional background checks to verify financial integrity before committing to high-stakes ventures.

What Defines a Financially Irresponsible Business Partner?

Financial irresponsibility is rarely a one-time error. It is a persistent failure to manage resources according to established fiduciary standards and high-quality corporate governance. In a professional ecosystem, this behavior manifests as a total disregard for the long-term health of the company in favor of short-term gratification or poorly calculated gambles. You must distinguish between temporary cash flow issues, which affected many firms when SBA 7(a) variable loan rates hit 13.25% in May 2026, and chronic, systemic mismanagement. The former is a market challenge; the latter is a character flaw that creates an unstable foundation for any venture.

Identifying the signs of a financially irresponsible business partner requires an investigative lens. We view this as “curated risk” management. Just as you would use a vetted integration for your CRM, you must filter potential partners through a rigorous discovery process. Personal financial habits serve as the primary predictor of professional fiscal conduct. If an individual cannot maintain a personal FICO score above the 680 threshold required for competitive 2026 lending rates, they’re unlikely to respect the company’s capital with the necessary discipline. This lack of boundaries between personal chaos and professional duty is where the most significant liabilities begin.

The Difference Between Risk-Taking and Recklessness

Calculated business risk relies on data, transparency, and a clear exit strategy. Recklessness, however, is driven by impulse. You might see a partner push for “growth at all costs,” but this often masks fundamental irresponsibility. In February 2026, Subchapter V bankruptcy filings saw a 91% increase, often because leaders prioritized expansion over liquidity. A responsible partner provides full transparency into the ledger, while a reckless one hides behind complex jargon or defensive posturing. True risk-taking involves a plan to handle the 8% interest rate currently set for large corporate underpayments; recklessness simply ignores the obligation until the crisis arrives.

Why Your Partner’s Personal Debt is Your Business Problem

There is a direct psychological link between personal financial pressure and professional misconduct. When a partner faces mounting personal debt, the temptation to cut corners or “borrow” from company accounts increases exponentially. Their creditors don’t just stay in the personal realm; they can disrupt company operations, trigger audits, or tarnish your brand’s reputation through association. Fiduciary duty is the strict legal and ethical obligation of a partner to act solely in the best interest of the business and its stakeholders. When personal debt compromises this duty, the entire partnership is at risk. Utilizing corporate due diligence is the only way to verify that a partner’s private life won’t sink your professional future.

Behavioral Red Flags: Identifying the ‘Hound’ Traits of Irresponsibility

Identifying the signs of a financially irresponsible business partner often begins with observing their relationship with status and accountability. One of the most dangerous patterns is the ‘Lifestyle Creep’ trap. This occurs when a partner upgrades their personal vehicle, residence, or wardrobe before the business has achieved sustainable profitability. In 2025, total bankruptcy filings rose by 11%, frequently driven by individuals who prioritized personal optics over operational liquidity. If your partner is spending as if the company has already succeeded, they’re likely treating the business account as a personal ATM rather than a growth engine.

Watch for the ‘Bailout’ pattern. This is a chronic history of relying on family, friends, or previous venture partners to resolve financial shortfalls. A partner who has never faced the consequences of their fiscal mistakes lacks the “financial scar tissue” necessary to manage a company through lean periods. They often possess a get-rich-quick mindset, seeking shortcuts or speculative “pivots” instead of focusing on the disciplined optimization required to scale. This behavioral profile is a precursor to workplace misconduct, as the pressure to maintain an inflated lifestyle eventually leads to ethical compromises. Performing due diligence on potential partners is the only way to uncover these historical patterns before they become your liability.

Communication Gaps and Financial Secrecy

Defensive or evasive communication regarding money is a tier-one warning sign. If a partner insists on “handling the books” alone or becomes irritable during routine budget reviews, they are gatekeeping critical data. This secrecy often masks underlying issues like unpaid payroll taxes or unauthorized draws. A “don’t worry about the details” attitude is not a sign of efficiency; it’s a sign of a lack of transparency. Professional clarity requires that all stakeholders have real-time access to financial integrations and bank statements. If you’re feeling locked out, it’s time to consider a formal corporate due diligence investigation to verify the ledger’s accuracy.

Impulsive Decision-Making and Lack of Planning

Impulsivity is the enemy of a healthy balance sheet. You can spot this through frequent, unplanned capital injections required for sudden “opportunities” that lack a vetted ROI. Financially irresponsible partners rarely maintain a professional emergency fund, leaving the business vulnerable when market conditions shift. In May 2026, with SBA 7(a) fixed rates reaching 14.75%, the cost of impulsive borrowing is higher than ever. Look for “impression-based spending,” such as high-end office build-outs or premium SaaS subscriptions that the current team doesn’t actually need. These are not growth investments; they are symptoms of a partner who values the feeling of success over the reality of it.

Operational Indicators: When Irresponsibility Hits the Ledger

Behavioral red flags eventually manifest as operational failures. When you transition from observing personality to auditing the ledger, the signs of a financially irresponsible business partner become undeniable. One of the most glaring indicators is a pattern of inconsistent vendor payments. If you hear “the check is in the mail” or excuses about banking glitches, you’re likely witnessing a liquidity crisis. These small operational leaks often point to a systemic failure to manage cash flow against the Q2 2026 IRS corporate underpayment rate of 6%.

Payroll disruptions represent the absolute ethical and legal line that an irresponsible partner will cross. With nearly 20 states increasing their minimum wage effective January 1, 2026, operational costs have tightened for many firms. An irresponsible partner might treat employee withholdings or tax reserves as a short-term loan to cover other debts. This is a fatal error. Co-mingling personal and business funds is the death knell for corporate protection. It invites creditors to pierce the corporate veil, making you personally liable for their mistakes. Unexplained expense reports, even for small amounts, indicate a fundamental lack of accountability that will eventually scale into larger losses.

The Vendor and Supplier Relationship Test

Strained relationships with long-term partners are a diagnostic tool for internal health. Pay attention if a supplier suddenly changes your terms from “net-30” to “COD” (Cash on Delivery). This shift indicates that your partner has burned through the company’s credit reputation. A partner’s standing with service providers mirrors their reliability within the firm. If they can’t manage a simple service contract, they won’t manage your company’s future with the necessary discipline.

Tax Compliance and Regulatory Filing Delays

Ignoring 1099 or W-2 filing deadlines is not just a clerical error; it’s a high-stakes gamble. The IRS has set the rate for large corporate underpayments at 8% for the second quarter of 2026. Borrowing from payroll tax withholdings to fund operations is a common tactic for desperate partners, but it carries severe personal penalties. A thorough corporate due diligence investigation is the most efficient way to uncover hidden tax liens or regulatory delays before they trigger a full-scale audit. Don’t wait for a federal notice to confirm your partner’s recklessness.

The Legal and Liability Risks of an Irresponsible Partner

When operational red flags are ignored, the situation inevitably transitions into the legal arena. The signs of a financially irresponsible business partner are no longer just internal headaches; they become catalysts for personal asset exposure. One of the most significant threats is the concept of “piercing the corporate veil.” If a partner treats the business as their “alter ego” by co-mingling funds or ignoring corporate formalities, a court can strip away your LLC or corporate protections. This means your personal savings, home, and investments are suddenly at risk for the debts of the partnership.

Joint and several liability further complicates this risk. In many partnership structures, you’re 100% responsible for the entirety of the company’s debt, regardless of your 50% ownership stake. If your partner triggers a default on a leveraged loan, which saw a 5.1% default rate in February 2026, creditors will pursue whoever has the liquid assets. This financial recklessness often evolves into criminal workplace misconduct, such as embezzlement or unauthorized use of credit lines. A breach of fiduciary duty provides the necessary legal grounds for dissolution, but the damage to your reputation and credit score may take years to repair.

Understanding Piercing the Corporate Veil

Business litigation frequently utilizes the “alter ego” theory to hold individual partners accountable for corporate liabilities. Poor record-keeping and a lack of distinction between personal and professional finances are the primary drivers of this exposure. With the Delaware Limited Liability Company Act amendments taking effect on August 1, 2026, the complexity of series LLCs and mergers requires even stricter adherence to corporate governance. In partnership lawsuits, the risk of personal asset seizure is high if the corporate structure is deemed a mere facade for a partner’s irresponsible spending.

The Domino Effect of Fraud and Misconduct

Reputational damage often follows a partner’s public financial failure, making it difficult to secure future financing or vendor contracts. Early intervention is critical. Professional workplace investigations help identify the initial indicators of internal theft or unauthorized draws before they escalate into systemic fraud. Distancing yourself from a partner’s reckless actions requires a proactive legal strategy and documented evidence of your own due diligence. If you suspect your partner’s habits have crossed the line into misconduct, request a professional corporate due diligence review to protect your personal interests.

Proactive Mitigation: Vetting for Financial Integrity

Identifying the signs of a financially irresponsible business partner is the first step toward securing your company’s future. However, awareness must lead to action. Vetting a potential partner requires the same level of scrutiny you would apply to a major software integration or a high-stakes merger. Passive observation is insufficient for a modern professional environment. You must implement a curated investigative process that filters out high-risk individuals before they gain access to your capital or credit. This proactive approach transforms anxiety into objective data, allowing you to make informed decisions with quiet confidence.

Mandatory pre-partnership background checks are a non-negotiable requirement for any venture. While basic HR software might catch recent criminal records, it often misses the nuanced history that a professional investigator uncovers. You need a deep dive into public records to identify hidden bankruptcies, pending civil litigations, or a trail of failed entities. In 2025, total bankruptcy filings increased by 11%, and many of these cases involved individuals who successfully masked their financial distress from casual observers. A professional review analyzes credit histories, looking for a Dun & Bradstreet PAYDEX score below 80 or a personal FICO score that fails to meet the 680 threshold required for competitive 2026 lending rates.

Establishing a “Business Prenup” or exit strategy is equally critical. This legal framework should clearly define the procedures for dissolution in the event of financial mismanagement or a breach of fiduciary duty. Implement structural safeguards such as dual-signature requirements for any expenditure over a specific dollar amount and mandate third-party audits of all company ledgers. These systems ensure that no single partner can jeopardize the firm’s liquidity without immediate detection. By building these check-and-balance systems into your operating agreement, you create an environment where transparency is the default setting rather than a point of contention.

The Role of Professional Background Screening

Professional pre-employment background checks are essential for key partners, not just entry-level staff. These screenings reveal if a partner has a history of “lifestyle creep” or impulsive spending that led to previous business failures. Utilizing professional skip tracing can locate former associates to provide vetted character references that go beyond a standard resume. This level of discovery is vital for identifying the systemic behavioral traits that predict future recklessness.

Implementing Structural Safeguards

Maintain real-time, transparent access to all company accounts and financial integrations. This ensures that every stakeholder can monitor the ledger without needing permission from a “gatekeeper.” Consider utilizing professional investigators for periodic “health checks” on your corporate due diligence to ensure no new liens or defaults have occurred. This ongoing monitoring acts as a specialized expert filter for your business interests. To ensure your next venture is built on a stable foundation, contact HubHound to vet your next business partnership today.

Protect Your Professional Assets with Strategic Vetting

A business partnership is a high-stakes integration that requires constant optimization and transparency. You’ve learned that the signs of a financially irresponsible business partner often begin in the personal realm before scaling into operational crises. Whether it’s the 91% increase in Subchapter V bankruptcy filings or the rising 6% IRS corporate underpayment rate, the economic landscape of May 2026 demands a rigorous defense strategy. You must prioritize structural safeguards and legal clarity to ensure your personal assets aren’t stripped away by a partner’s reckless spending or poor record-keeping.

Don’t leave your company’s future to chance or “gut feelings.” Our team of licensed investigators brings 30+ years of experience to every case, utilizing vetted and verified investigative techniques to uncover hidden liabilities. We specialize in corporate due diligence and asset searches that provide the hard evidence you need to act. Secure your company’s future with professional due diligence from HubHound. With the right data in hand, you can lead your enterprise toward sustainable growth and long-term stability.

Frequently Asked Questions

Can I be held liable for my business partner’s personal debt?

You are generally not liable for a partner’s personal debt unless a creditor successfully pierces the corporate veil. This occurs when the legal boundary between personal and business finances is blurred through co-mingling funds. If a partner uses company accounts for personal expenses, creditors may argue the business is an “alter ego” of the individual. This exposes your personal assets to their private liabilities during litigation.

What should I do if I suspect my business partner is stealing?

Secure all financial records and contact a professional investigative firm immediately if you suspect internal theft. Do not confront the individual until you have compiled objective evidence through a formal workplace misconduct investigation. Unauthorized changes to banking credentials or missing digital receipts are critical pieces of data. Maintaining a chain of custody for this evidence is vital for any potential civil litigation or criminal referral.

Is it legal to run a background check on a potential business partner?

It is entirely legal to run a background check on a potential partner as part of your due diligence process. You must ensure compliance with federal regulations regarding consent and data usage before beginning the search. Vetting for the signs of a financially irresponsible business partner before signing an operating agreement is a standard professional practice. This process helps identify hidden tax liens or a history of failed ventures that a simple resume would omit.

What are the most common signs of embezzlement in a small business?

The most common signs of embezzlement include unexplained discrepancies in bank reconciliations and frequent, small unauthorized withdrawals. Look for vendors with names similar to known suppliers or payments that lack corresponding invoices. In 2025, commercial bankruptcy filings rose by 5%, often precipitated by internal fraud that drained liquidity before the owners noticed the “leaks” in their expense reports.

How do I confront a partner about their financial irresponsibility?

Initiate the conversation by presenting specific, documented financial discrepancies rather than personal opinions. Use objective benchmarks, such as the 8% interest rate for large corporate underpayments, to explain why their management of company funds is a risk to the firm’s survival. Focus on the impact to the company’s credit score and its ability to secure future SBA loans. Professionalism reduces the likelihood of defensive posturing during these high-stakes discussions.

What is the difference between a credit check and a professional due diligence report?

A credit check provides a numerical risk score, while a professional due diligence report uncovers the context behind those numbers. While a lender might look for a minimum FICO score of 680, an investigator searches public records for undisclosed litigations, civil judgments, and previous business failures. Due diligence utilizes skip tracing and witness interviews to verify a partner’s professional reputation beyond their credit history.

Can financial irresponsibility be a valid reason to dissolve a partnership?

Financial irresponsibility is a valid reason for dissolution if it results in a breach of fiduciary duty. Most operating agreements include clauses that allow for the removal of a partner who jeopardizes the company’s legal or financial standing. With the August 1, 2026, amendments to the Delaware LLC Act, maintaining strict corporate governance is more critical than ever. Chronic mismanagement provides the legal foundation needed to protect the business from further harm.

How often should a business conduct internal financial investigations?

Conduct internal financial “health checks” or investigations at least once every six months to maintain operational integrity. These reviews should coincide with Q2 and Q4 tax periods to ensure compliance with changing IRS interest rates, such as the 6% rate for corporate underpayments. Regular audits act as a deterrent for misconduct and ensure that small accounting errors don’t evolve into systemic financial crises.